India In Sight #105

Weekly updates on Indian private markets. Featuring reports on 'Pre-Seed funding landscape in India' by Eximius Venture and '3D Printing in Healthcare' by Kalaari Capital

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs, and top tier research

Search, screen, filter, and save - all reports at one spot! Subscribe to India In Sight Library

Subscribe to receive the newsletter every week in your inbox! Stay informed, stay ahead!

Key reports in this edition:

Indian Startup H1-2025 by Entrackr

Pre-Seed funding landscape in India by Eximius Venture

3D Printing in Healthcare by Kalaari Capital

Power Transmission & Distribution (T&D) sector report by InVed

Insurance sector thematic report by HDFC

India Market Outlook - June 2025 by Morgan Stanley

KEY DEALS

Equity

Bambrew, a producer of sustainable packaging materials, raised c.$10 million in its latest Series B funding round led by Ashok Goel (ex-MD, Essel Propack) and Enrission India Capital, a Japan-based VC firm. (July 02, 2025)

AppsForBharat, a parent company of devotional platform Sri Mandir, raised c.$20 million in its Series C funding round led by Susquehanna Asia Venture Capital. Other investors include Fundamentum, Elevation Capital, and Peak XV Partners. (July 01, 2025)

Eeki, a sustainability focused agritech startup, raised c.$7 million from Sixth Sense Ventures. (July 01, 2025)

Jumbotail, a B2B marketplace for food and groceries, raised c.$120 million in its funding round led by SC Ventures and Artal Asia. (June 30, 2025)

Aukera, a lab-grown diamond jewellery brand, secured a commitment of c.$15 million in its Series B funding led round by Peak XV. Other investors include Fireside, Sparrow Capital, Prath Ventures, and Alteria Capital. (June 30, 2025)

Credit

InCred Finance, InCred Group’s lending arm, raised a debt funding of c.$47 million from Morgan Stanley and Nippon Life India. InCred Capital, its parent company, also infused c.$5 million in equity funding. (July 03, 2025)

FincFriends, an NBFC, raised c.$12 million in debt funding from NBFCs and NCDs, which saw the participation of IBL Finance, InCred Financial, Real Touch Finance, and Western Capital Advisors. (July 01, 2025)

Infra.Market, a B2B construction materials marketplace, raised an additional c.$50 million in debt financing from Mars Growth Capital ahead of its IPO. (June 30, 2025)

MARKET INSIGHTS & RESEARCH

Reports

Entrackr’s report ‘Indian Startup H1-2025’ outlines that Indian startups raised $6.7B in H1 2025 across 550+ deals. Growth and late-stage deals dominated with $5.1B (148 deals), while early-stage rounds saw $1.5B in funding. Fintech saw highest investment with $1.5B. Notable activity included 5 new unicorns, 10 $100M+ late-stage deals with a surge in IPO activities.

Eximius Venture’s report on ‘Pre-Seed funding landscape in India’ notes that India’s pre-seed funding ecosystem saw deal activity rising by 10.5% in 2023 despite a broader slowdown. 50K+ startups now exist, and key sectors attracting early capital include fintech, healthtech, deep tech, and consumer. Cheque sizes range from $50-500K, with growing interest from global investors and second-time founders.

Kalaari Capital’s report on ‘3D Printing in Healthcare’ highlights that the medical 3D printing market is expected to grow to $11B by 2032, driven by innovations in personalized prosthetics, implants, bioprinted tissues, and drug delivery. With over 300K patients awaiting organ transplants in India and a 90% mismatch rate in cities like Mumbai, 3D bioprinting offers a path to address this gap.

InVed’s report on ‘Power Transmission & Distribution (T&D) Sector’ expects investments to rise from $5.9B in FY24 to $14.1B by FY30. The need to integrate 500 GW of renewable energy by 2030, reduce AT&C losses (~15%), and modernize an aging grid is driving this surge, with shifting focus from generation to grid infra. c.$9B worth of tenders already floated under the revamped DISCOM scheme.

HDFC’s thematic report on ‘Insurance sector’ projects life insurance premiums to rise from $96B in FY24 to $200B+ by FY33 (11% CAGR), and non-life premiums to grow from $42B to $130B+ (13% CAGR). Strong tailwinds exist—like underpenetration (4% vs global avg. of 7%) and favorable demographics. Key drivers include rising affluence, regulatory push (IRDAI’s “Insurance for All” by 2047), and improved distribution.

Standard Chartered’s ‘India Market Outlook’ for June 2025 remains optimistic, with GDP growth projected at 6.7% for FY26, driven by strong investment momentum, controlled inflation (~4.5%), and robust manufacturing and infrastructure activity. Key sectoral trends include opportunities in banking, capital goods, autos, and consumption.

Motilal Oswal’s report on ‘The Crossover Quarter’ expects India to deliver a steady Q1FY26 performance, with Nifty 50 PAT likely to grow by 10% YoY, led by BFSI, autos, and capital goods. Revenue growth for the quarter is estimated at ~7% YoY, with EBITDA rising ~11% and margins expanding by ~40 bps. Autos and banks will drive earnings growth, while sectors like oil & gas and IT may face headwinds.

PWC’s report on ‘Eight years of GST’ highlights strong progress, with average monthly collections doubling from FY18 to FY25, peaking at $27.9B in April 2025—a 12.6% YoY rise. E-invoicing, AI-based audits, and real-time data integration have driven this growth. Key reforms include operationalising the GST Appellate Tribunal, clarifying tax rules, and launching a GST waiver scheme to reduce litigation.

Check out our 100th Edition Special for the top reports so far in 2025!

Articles

In H1 2025, VC funding in Indian startups rose by 9% YoY to c.$5B across 410 deals (vs 418 deals in H1 2024), signaling a modest recovery. Early-stage activity remained robust, suggesting a return to normalized funding levels. Read more.

In FY25, Indian corporates increasingly turned to capital markets, with total resource mobilisation rising by 32.9% to c.$185B. Fundraising was led by debt instruments, esp. private placements, with strong equity activity. Read more.

Alternative Investment Funds (AIFs) are playing an increasingly critical role in India's real estate sector by bridging funding gaps for land acquisition and project completion, enabling faster project launches, timely delivery, and growing investor interest. Read more.

Indian investors are increasingly turning to bonds as a stable and diversified investment option, supported by the rise of digital platforms and growing retail participation. Corporate bond issuance is on the rise, but India’s corporate debt market still holds significant untapped potential. Read more.

India’s luxury market is expected to grow from $75B in 2022 to $200B by 2030, driven by cultural richness, rising affluence beyond metros, and demand for authentic, values-led brands. Hospitality and weddings present untapped avenues for experiential luxury, offering India a unique opportunity. Read more.

India’s retail real estate is evolving from transactional spaces to immersive, experience-driven destinations. Malls and high streets are becoming hubs for entertainment, with entertainment zones now occupying ~15% of tenant mixes. Focus is on flexible layouts, interactive experiences, and brand story. Read more.

The Motor Vehicle Aggregator Guidelines 2025 officially legalized dynamic pricing for ride-hailing platforms like Ola, Uber, and Rapido—allowing fares up to 2x during peak hours and 50% discounts in off-peak times, while base fares remain state-regulated. Drivers to earn ~80% of fares on their own vehicles and 60% when using aggregator-owned ones. Read more.

India is emerging as a global hub for AI deployment through its vast services sector, deep talent pool, and rapidly expanding GCC network. India needs to invest heavily in talent, research, and innovation to improve in AI. Read more.

KPIs

New private sector project announcements in India dropped to a four-quarter low in Q1 FY26. However, overall investments more than doubled YoY to $41B, led by Odisha. Slowdown in project count were driven by tariff uncertainties and weak domestic demand, which have tempered capacity expansion plans.

Industrial production fell to nine-month low of 1.2% in May 2025. Core sector growth also slumped to a nine-month low of 0.7% in May vs 1% in April 2025.

Gross GST collections doubled in five years to reach an all-time high of c.$260B in the 2024-25 fiscal year, vs $133B in FY21 (up ~10% YoY). In eight years, the number of registered taxpayers under GST went up from 650K in 2017 to 15M+.

India needs to sustain an average nominal GDP growth of 10% annually to realize its Viksit Bharat vision by 2047. Upcoming interim trade deal with the US will reduce uncertainty and open up greater market access for Indian businesses.

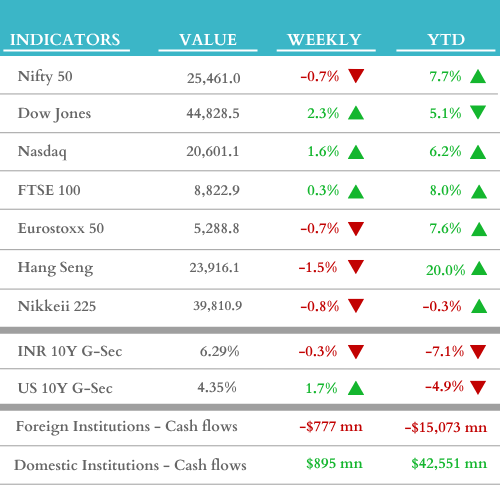

WEEKLY MARKET UPDATE (w/c June 30, 2025)

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.