India In Sight #108

Weekly updates on Indian private markets. Featuring 'PE/VC 1H2025 Roundup' by EY IVCA and 'Indian PE deals and landscape' by Khaitan & Co.

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs, and top tier research

Search, screen, filter, and save - all reports at one spot! Subscribe to India In Sight Library

Subscribe to receive the newsletter every week in your inbox! Stay informed, stay ahead!

Key reports in this edition:

PE/VC 1H and June 2025 Roundup by EY IVCA

What’s Market in Indian PE deals by Khaitan & Co

The Resilient Reset of India’s Microfinance Sector by Avendus

Global Capability Centres 2025 by Dhruva Advisors

Crypto investing in India by HDFC Securities

Healthcare BPO sector report by Aditya Birla Capital

Indian Wealth Management sector report by Bernstein

KEY DEALS

Equity

[Expected] Multiples Equity, an alternate asset management company, looking to acquire a c.32% stake in VIP Industries, a luggage and travel accessories maker, from Piramal family. The transaction would trigger an open offer to buy additional 26% and hence awaiting CCI approval. (July 27, 2025)

EatClub, a cloud kitchen operator, to raise c.$22 million from Tiger Global, A91 Partners, and 360 One. (July 25, 2025)

Netrasemi, a semiconductor startup, raised c.$13 million from Zoho and Unicorn India Ventures. (July 24, 2025)

[Exit] Canada Pension Plan Investment Board (CPPIB) to sell its c.49% stake in the investment platform with The Phoenix Mills, a real estate and mall developer, for c.$631 million, to be paid in four tranches over 3 years. (July 24, 2025)

SuperK, a branded supermarket chain, raised c.$12 million in its Series B funding round led by 3STATE Ventures and Mithun Sancheti (CaratLane founder). (July 24, 2025)

Gupshup, a conversational AI platform, raised c.$60 million in equity and debt funding from Globespan Capital Partners and EvolutionX Debt Capital. (July 23, 2025)

Kumar Vibe Properties, a real estate firm, raised c.$13 million from Nisus Finance for the development of its projects in Mumbai and Pune. (July 23, 2025)

[Exit] Bain Capital sold c.3.7% stake in 360 ONE WAM, a wealth management firm, for c.$200 million through an open market transaction. (July 22, 2025)

Composio, an agentic AI startup, raised c.$25 million in a funding round led by Lightspeed. Other investors include Elevation Capital, Together Fund, and angel investors. (July 22, 2025)

[Expected] IndusInd Bank is looking to raise c.$3.5 billion through equity and debt instruments. (July 23, 2025)

KEY FUNDS AND FUNDRAISES

Yali Capital, a VC firm, marked a final close of its first deeptech fund at c.$100 million. (July 25, 2025)

Motilal Oswal Alternates marked the final close of its sixth real estate fund at c.$230 million. (July 23, 2025)

Amicus Capital, a domestic PE fund, marked the final close of its second fund at c.$214 million, exceeding its initial target of c.$200 million. (July 23, 2025)

MARKET INSIGHTS & RESEARCH

Reports

EY IVCA’s ‘PE/VC Monthly Roundup’ report shows that in 1H2025, India recorded $26.4B in PE/VC investments—down 19% YoY but up 11% from 2H2024. Pure-play PE/VC funding dipped 3% YoY to $18.3B, while real estate and infrastructure investments fell sharply by 40% YoY. However, compared to 2H2024, both segments showed modest recovery. Start-up investment deals emerged as the highest at $6.8B, followed by growth investments at $6.5B.

Khaitan & Co’s report on ‘India’s PE market and deals’ highlights that the Indian PE market showed resilience in 2024–2025, with strong activity in infrastructure, tech, and financial services. Large deals led by foreign funds saw a rise, with a preference for minority stakes and increased PE-backed IPOs and exits. ESG focus and the use of Singapore arbitration for disputes also gained prominence.

Avendus’ report on ‘The Resilient Reset of India’s Microfinance Sector’ highlights a strong post-COVID recovery, with the sector growing at a 27% CAGR since FY21 to reach $44B in FY24. Key drivers include improved borrower behavior, regulatory clarity, and strong rural credit demand. NBFC-MFIs now command 42% market share, up from 31% in FY21. The top 10 MFIs account for over 75% of the segment’s AUM.

Dhruva Advisors’ report ‘Global Capability Centres 2025’ highlights the continued growth of GCCs in India, with over 1,580 centres employing more than 1.9M professionals and contributing ~$46B to exports. India remains a top destination due to talent availability, digital maturity, and cost efficiency. Emerging GCC trends include increased focus on ESG, GenAI integration, and hybrid work models.

HDFC Securities’ report on ‘Crypto investing in India’ highlights that crypto investing is growing in India, driven by youth, HNIs, and global momentum, but faces world’s harshest tax regimes — 30% tax on gains and 1% TDS on transactions. While Bitcoin outperformed traditional assets with a 10Y CAGR of 82% vs. 11% for Nifty 500, systemic risks like custody issues, cyberheists, & lack of SEBI/RBI oversight persist.

Aditya Birla Capital’s report on ‘Healthcare BPO’ highlights India’s growing role in the $300B+ global healthcare outsourcing market, driven by cost efficiency, skilled workforce, and digital adoption. The Indian Healthcare BPO sector is expected to grow at a 12–14% CAGR, with segments like medical billing, claims processing, and telehealth support seeing strong demand. India’s advantage lies in scale, time-zone alignment, and tech-enabled delivery, making it a strategic hub for global healthcare operations.

Bernstein’s report on ‘Indian Wealth Management sector’ projects strong growth for India’s wealth management industry, with AUM expected to rise at a 15%+ CAGR over FY24–30, driven by HNIs, financialization of assets, and digital adoption. The market remains fragmented, offering scope for consolidation. Fee-based advisory and alternates are gaining traction, with RIAs and tech platforms reshaping engagement.

Articles

India’s credit ecosystem is evolving from traditional collateral-based lending to a data-driven, inclusive framework enabled by Digital Public Infrastructure (DPI). Initiatives like Account Aggregator, OCEN, and the forthcoming Unified Lending Interface (ULI) are enhancing credit delivery efficiency. Read more.

Estimating disinvestment receipts for FY26 is challenging due to multiple variables. The $5.5B target includes various monetization routes beyond traditional disinvestment. Profitability is not a primary criterion in privatisation decisions. Read more.

IPO fundraising in H1 2025 surged 45% YoY to c.$5.3B, despite global uncertainties, driven by larger deal sizes as the number of IPOs fell to 24 from 36. This points to a rise in average issue size. Experts expect the IPO market to remain cautiously optimistic in H2 2025. Read more.

Government is exploring AI-driven solutions to resolve persistent delays in the National Single Window System for investors. Industry concerns over processing bottlenecks have prompted DPIIT to evaluate AI enhancements to streamline multiple-clearance applications and status tracking. Read more.

KPIs

India’s rural economy is witnessing robust growth, driven by better agricultural output, government support, and rising rural consumption—now outpacing urban demand. Unemployment is falling, tractor sales are set to hit record highs, and FMCG and small manufacturers are seeing faster expansion in rural areas.

India’s employment scenario has improved notably, with the number of employed individuals rising from 4.7B in FY18 to 6.4B in FY24. The Labour Force Participation Rate and Worker Population Ratio also increased, while overall and youth unemployment rates declined.

Following the RBI’s repo rate cut, public sector banks have reduced lending and deposit rates more sharply than private banks. Lending rates on fresh loans dropped significantly, while some public banks lowered savings deposit rates to their lowest levels since deregulation.

India’s debt grew at a slower pace than GDP between FY21 and FY23, indicating improved debt sustainability. The Centre’s debt-to-GDP ratio declined from its pandemic peak to 57.93% in FY23. Better debt repayment also allowed more borrowings to be directed toward productive expenditure.

India’s economy held steady in June–July despite global uncertainties, buoyed by a favorable monsoon, strong services performance, and moderate industrial growth. CPI inflation remained below 4% for the fifth consecutive month, driven by declining food prices.

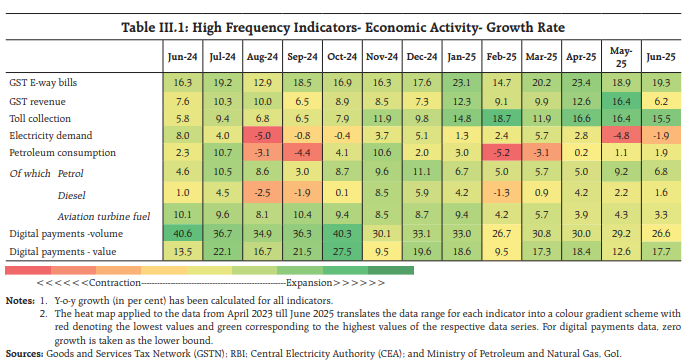

Below is a quick snapshot of the services sector performance from the latest RBI bulletin July 2025.

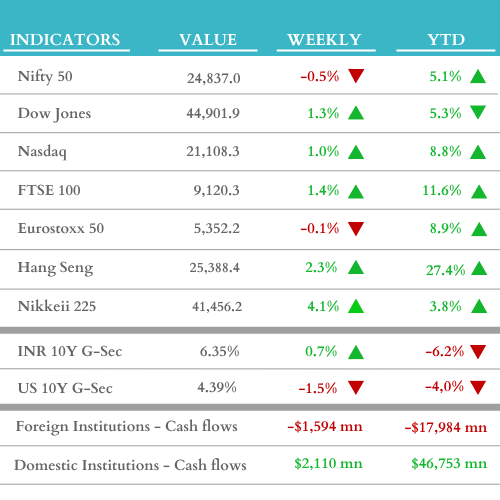

WEEKLY MARKET UPDATE (w/c July 21, 2025)

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.