India In Sight #54

Weekly updates on Indian private markets

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity. Deeply embedded in the private markets ecosystem, ACP works with large global institutions to provide creative capital solutions for companies and asset managers.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs and top tier research.

Subscribe to receive the newsletter every week in your inbox!

Stay tuned, Stay ahead!

Key reports in this edition:

Future Unicorn Index 2024 by Ask Private Wealth and Hurun India

Indian domestic formulations by Avendus

The new India – Infrastructure: An ongoing transformation by Morgan Stanley

Agrochemical cycle at the cusp of a turnaround! by ICICI Securities

Sector notes on oil & gas (Nirmal Bang), hotel sector and capital goods (Motilal Oswal)

India growth story 2023-2024 by Fibonacci X

KEY DEALS

Equity

Zepto, an online grocery delivery and quick commerce app, raised c.$665 million in a fresh round of funding led by Glade Brook, Nexus, and Stepstone for an estimated valuation of c.$3.6 billion (up from previous valuation of $1.4 billion). Existing and new investors include Goodwater, Lachy Groom, Avenir, Lightspeed, and Avra. (June 21, 2024)

[Exit] General Atlantic and Ares Asia sold c.2.5% stake each in PNB Housing, a housing finance company, for c.$60 million each. (June 20, 2024)

[Exit] Olympus Capital Asia, a PE firm, to sell its c.10% stake in Aster DM Healthcare, a healthcare ed-tech company, in a block deal for c.$200 million. (June 20, 2024)

Omega Hospitals, a cancer-focused hospital chain, raised c.$60 million from Morgan Stanley Private Equity Asia. The funds will be used to expand the hospital’s footprint across India. (June 19, 2024)

Ummeed Housing Finance, a digital housing finance company, raised $75 million in a Series F round from A91 Partners, Mirae Asset Venture, Anicut Capital, and existing investors Norwest Venture Partners. (June 19, 2024)

ESR India, a warehousing and logistics-focused real estate manager and a JV between ESR Group and Allianz Real Estate, acquired 27 acres of land in a Chennai-based industrial park, for c.$33 million. (June 18, 2024)

[Expected] Whatfix, a SaaS firm, to raise c.$100-$150 million from Warburg Pincus at an estimated valuation of c.$800 million. Other investors include Softbank, Helion Venture Partners, and Eight Roads Ventures. (June 19, 2024)

[Expected] Career Mosaic, an domestic student consulting firm that operates globally, is looking to raise c.$30 million from private equity investors for a minority stake. (June 20, 2024)

Credit Deals and Issuances

REC, a state-owned power financier, is looking to raise c.$500 million through the issuance of green bonds from overseas investors. The proceeds will be used to fund renewable energy projects. (June 21, 2024)

Nisus Finance, a domestic real-estate investor, invested c.$18 million in Surat’s Swaminarayan Green City, developed by Dharmadev Group, a residential & commercial construction company, from its c.$85 million stressed assets fund. (June 20, 2024)

Hinduja Group, an Indian diversified conglomerate, is looking to raise c.$875 million via two rupee-bond offerings to finance its acquisition of Reliance Capital. (June 20, 2024)

Vedanta, a mining company, is looking to raise c.$120 million via NCDs in a private placement. (June 20, 2024)

Bank of Maharashtra, is looking to raise c.$120 million through the issuance of 10-year tier-II bonds. (June 19, 2024)

Aye Finance, a microlending platform, raised c.$30 million in debt from FMO. The funds will be used to extend loans to underserved MSMEs across India. (June 19, 2024)

KEY FUNDS AND FUNDRAISES

Capria Ventures, a US-based venture capital firm, is looking to raise c.$125 million for its latest India-focused fund. (June 20, 2024)

General Catalyst, a global venture capital fund, acquired Venture Highway, an India focused early-stage investor. As part of this move, Venture Highway—which has backed unicorns like Meesho and Moglix—will cease to exist and will transition into General Catalyst India. (June 20, 2024)

GVFL Ltd, a venture capital firm, marked the first close of its latest investment vehicle at c.$12 million. The fund has a target corpus of c.$25 million. The fund will invest in seed-stage startups in India. (June 19, 2024)

BPEA Credit, an Asia-focused credit investor, marked the first close of its India-focused rupee-denominated fund at an estimated c.$50 million. The fund has a target corpus of $90 million. (June 19, 2024)

Elev8 Venture Partners, a deep tech focused VC fund, which launched its maiden venture capital fund in 2023 with a target corpus of c.$200 million, is looking to mark the final close by the end of year. (June 19, 2024)

8X Ventures, an early-stage venture capital firm, marked the first close of its second VC fund at c.$7 million. The funds has a target corpus of c.$25 million. (June 19, 2024)

Z21 Ventures, an early-stage investment firm focused on India and US, is looking to raise c.$40 million for its second fund. The fund targets enterprise software and hardware startups, backed by a community of Indian-origin technology executives. (June 18, 2024)

Brookfield secured a commitment of c.$105 million in debt from IFC to invest in solar projects in western India. Brookfield is also looking to raise c.$5 billion overall for its climate-focused fund to invest in emerging markets. (June 17, 2024)

VentureSoul Capital, a domestic venture debt firm, launched its maiden fund with a target corpus of c.$70 million to invest across sectors in the new economy space. (June 17, 2024)

MARKET INSIGHTS & RESEARCH

Reports

Ask Private Wealth and Hurun India’s report ‘Future Unicorn Index 2024’ aims to highlight India's burgeoning start-up ecosystem. India now has 67 unicorns, 46 gazelles, and 106 cheetahs. The list saw 25 dropouts and 38 new entrants, with notable promotions including Zepto and Incred Finance to unicorn status. The index showcases start-ups with a minimum valuation of $200 million, and India's future unicorns are currently valued at $58 billion. Peak XV Partners remains the most active investor, while Agnikul achieved a milestone by launching India's first 3D-printed rocket.

Avendus report on ‘Indian domestic formulations’ highlights that India is the 3rd largest pharma market by volume and one of the fastest-growing, and has emerged as "the pharmacy to the world" with 25% of USFDA-approved plants outside the US. The Indian domestic formulations (DomForm) market is expected to touch c.$65 billion by 2034, growing at a CAGR of 10%. c.50% of local production is now for domestic consumption, with domestic-focused stocks outperforming export-oriented ones. Over the last 6 years, DomForm has attracted strategic and private equity investments worth c.$14 billion.

Morgan Stanley report ‘The new India – Infrastructure: An ongoing transformation’ highlights that India's infrastructure has significantly improved recently, with further enhancements expected through initiatives like PM Gati Shakti (PMGS). Infrastructure investments are projected to grow at a 15.3% CAGR, reaching $1.5 trillion over the next five years, enhancing manufacturing competitiveness by lowering logistical costs and boosting productivity.

ICICI Securities report ‘Agrochemical cycle at the cusp of a turnaround!’ shares that early signs of recovery in agrochemicals, particularly in supplies for innovators, are now evident after a challenging FY24. Inventory levels have dropped below normal, and steady demand, coupled with increased outsourcing by US agrochemical companies, benefits Indian specialty chemical firms. Estimates for Indian chemical companies have been downgraded in the past 18 months but are set to drive EPS growth over 25% in the next three years (FY24-27E).

Motilal Oswal's note on ‘hotel sector’ highlights that the hotel industry is experiencing strong performance driven by favorable demand-supply dynamics, with branded room demand expected to grow at a 10.6% CAGR over FY24-27, outpacing supply growth. Major players are focusing on management hotels and revenue diversification, while asset owners are expanding owned assets. Key growth drivers include infrastructure development, increased business and leisure travel, and growing theme-based tourism. For the key leisure market, demand is expected to witness a c.13% CAGR over FY24-27 vs. supply CAGR of 10%. Supply growth in the luxury/upper upscale segments is much lower at

c.5%/7% CAGR over FY23-27 vs. c.11% CAGR for the economy/midscale segment,

leading to better pricing power for premium players.

Nirmal Bang note on ‘oil & gas sector’ outlines that the oil and gas sector faces challenges with weak refining and retail margins expected to impact 1QFY25 for OMCs. The IEA forecasts a slowdown in global oil demand growth. Despite a rise in global oil supply, Asian refining margins have hit three-year lows, and US Gulf Coast refining profitability is also down. Indian petroleum demand showed a 1% yoy decline in May'24 but increased by 2.4% yoy for 1QFY25-QTD.

Motilal Oswal’s report on ‘capital goods’ provides insights that the genset market stands at c.$1.2 billion and the demand remained strong in 1QFY25, driven by pre-buying and steady demand across various segments. Key factors include: 1) demand from government contracts, railway projects, infrastructure and real estate; 2) data center-led demand is fairly strong; 3) price stabilization in the next one year as operating leverage kicks in; and 4) recovery in exports from current levels.

Colliers report on ‘Equitable growth and emerging real estate hotspots’ outlines that real estate development is expected to expand beyond tier I cities into 30 high-potential cities identified by Colliers, driven by infrastructure growth, tourism, and digital penetration. Key highlights include infrastructure as a catalyst for growth, evolving work models boosting commercial and residential activity in smaller cities, and growth in alternate assets like senior living and data centers due to spiritual tourism and digitization.

India growth story 2023-2024 report by Fibonacci X highlights that India's GDP has grown 6x over the past 20 years, making it the fifth largest economy globally. A report predicts India's growth to be in the 6-10% range in the coming years, driven by the services sector, R&D, and digital payments, while manufacturing growth remains stagnant, awaiting new policy outcomes. Agriculture continues to be the underperforming sector. Read more.

Articles

The Indian government has requested the central bank to exempt sovereign funds, including the Special Window for Affordable and Mid-Income Housing (SWAMIH), from tightened rules on alternate investment funds (AIFs) to support their socio-economic purposes. This follows the RBI's December directive for banks and NBFCs to increase provisions for AIF investments, which was partially eased in March. Read more.

Avendus' note ‘Is “Consumption” the new buzzword?’ details that following the June 4th General Elections, investors shifted focus to "Consumption" stocks. This trend was reinforced by the government’s $2.4 billion PM Kisan Nidhi Scheme, benefiting over 90 million farmers, and by India's FY24 GDP growth of 8.2%, with private consumption at 4% and Gross Fixed Capital Formation at 9%. Investors are encouraged to consider allocating to consumer-related sectors for potential growth.

Indian corporates are likely to slow down on overseas dollar loans due to high borrowing costs, with US rates at 5.25-5.50%. However, there is significant demand for local equity investments. Bank of America expects robust activity in Indian IPOs and M&A, despite recent market volatility and the slower recovery in Asia compared to the US. Read more.

PwC India expects a rise in market activity, particularly in small to mid-size M&A transactions and growth funding. PwC highlights various M&A strategies, PE investment trends, and notable deals. Key drivers include India's 'Viksit Bharat agenda, emphasizing emerging technologies and ESG integration. Read more.

India has formalized c.$310 billion of its economy in seven years, reducing the informal economy's share to 23.7% in FY23 from 25.9% in FY16. c.45% of the labor force remains informal, with agriculture (25.5%) and services (13.9%) contributing significantly. The e-Shram portal, registering 297 million unorganized workers, aims to accelerate this formalization. Notably, 44% of the population spends less than $3.65 per day, and private final consumption expenditure grew 4% in FY24 amid an 8.2% economic growth. Read more.

India’s 10-year bond yield has decreased by over 20 bps since the announcement of its inclusion in a global index. Fund managers anticipate an additional 25-30 basis point decline. The current drop is primarily due to demand from foreign investors, with further easing expected from potential policy rate cuts and fiscal prudence. Read more. [Paywall]

KPIs

India dropped seven ranks in the global FDI ranking, with inflows down 43% in 2023. Global FDI fell 2% to $1.3 trillion in 2023, with flows to developing countries dropping 7% to $867 billion. Tight financing conditions led to a 26% decline in international project finance deals. Among the top 20 host economies, the largest drops were in France, Australia, China, the US, and India.

India is rapidly becoming the most attractive consumer market globally, with consumption trends aligning with those of major cities. Middle India is projected to be 47% in 2030-31 and 61% in 2046-47. The services sector is anticipated to drive robust economic growth, positioning India as a global economic hotspot. While manufacturing growth has stagnated, future progress hinges on new policy initiatives.

As per the latest ‘RBI Bulletin’, India's GDP growth is steady, supported by favorable monsoon prospects and easing inflation, despite volatile food prices. In 2021-22, the Indian economy returned to a net borrower status, with household net financial wealth at 93.5% of GDP. Additionally, India’s deposit insurance system, celebrating 60 years, aims to enhance coverage, speed up claim settlements, and modernize infrastructure.

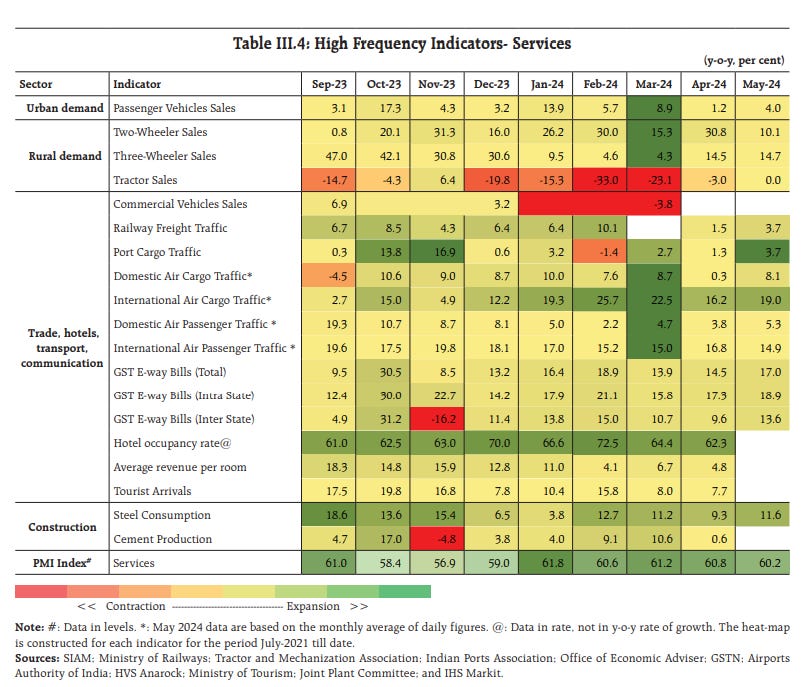

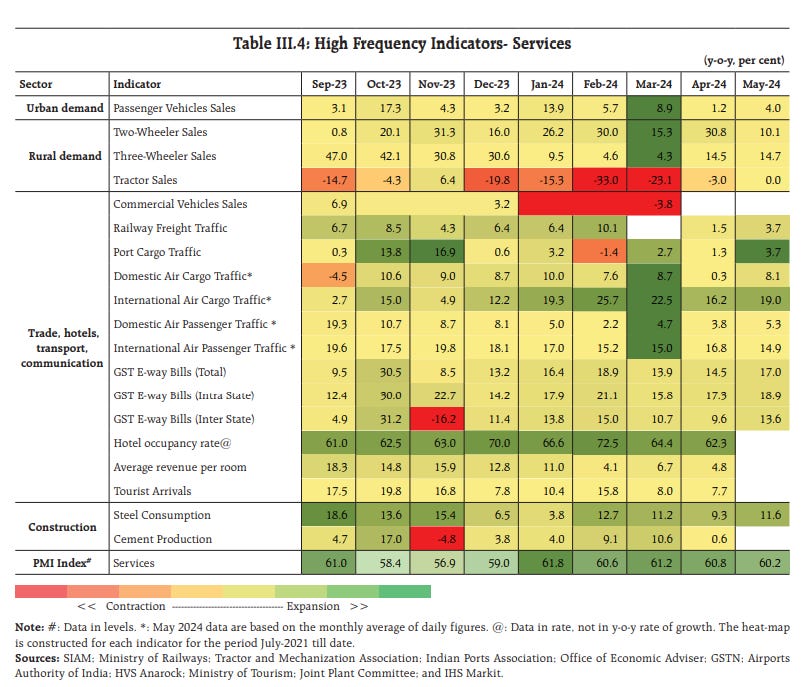

Below is a quick snapshot of the services sector performance from the latest RBI bulletin June 2024.

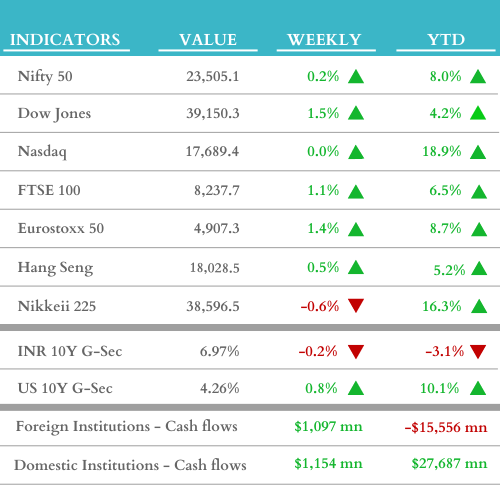

WEEKLY MARKET UPDATE (w/c June 17, 2024)

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.