India In Sight #55

Weekly updates on Indian private markets

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity. Deeply embedded in the private markets ecosystem, ACP works with large global institutions to provide creative capital solutions for companies and asset managers.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs and top tier research.

Subscribe to receive the newsletter every week in your inbox!

Stay tuned, Stay ahead!

Key reports in this edition:

Fuels of the future - Exploring alternative fuel options for transport by Deloitte

Unique’orn series: Indian textile sector by Avendus Spark

Indian alco-beverage market report by Technopack

The dichotomy of formalization research paper by State Bank of India

Sector notes on automobiles (by Ambit), India office occupier survey (by CBRE), pharma, ports & logistics (by ICRA)

KEY DEALS

Equity

[Exit] Oman India Joint Investment Fund (OIJIF), a mid-market private equity

firm, sold its remaining stake in Stanley Lifestyles, a designer and manufacturer of furniture brands, for c.$50 million in its IPO. OIJIF first invested c.$20+ million in the company in 2018 and has harvested c.$75 million till date (translating to 3.5x+ MOIC). (June 28, 2024)

India Resurgence Fund, an investment platform by Bain Capital and Piramal

Enterprises, sold its remaining c.7.4% stake in Archean Chemicals, a chemicals manufacturing company, for c.$72 million. The fund first invested $120+ million in the company in 2018 and generated c.$50 million by selling its 50% stake in 2022 during the company’s IPO. (June 27, 2024)

TPG to acquire a majority stake in Altimetrik, a digital business services company operating in India and US. The exact financial details were not disclosed. (June 27, 2024)

GIC, a Singapore sovereign wealth fund, invested c.$25 million in Affle, a mobile solutions and technology company, increasing its stake in the company to c.6% for c.$115 million. (June 27, 2024)

Finnest, a London-based PE firm, acquired a majority stake in Kitchens@, a cloud kitchen startup, for c.$160 million at a valuation of c.$305 million. (June 27, 2024)

Ontario Teachers Pension Plan ( OTPP) acquired a c.24% stake in Kogta Financial, an NBFC, for c.$150 million from Creador (c.2.5x MOIC) and Morgan Stanley (c.5x MOIC). (June 26, 2024)

Novo Holdings, a Danish investor, invested in AgNext Technologies, an Indian agritech company. The financial details of the transaction were not disclosed. (June 26, 2024)

[Exit] WestBridge Capital, Sixth Sense, and Convergent Finance sold their stake in Hindustan Foods, a contract food manufacturing services company, for a combined value of c.$75 million in a secondary market transaction. Westbridge invested c.$10 million in 2019 and has harvested c.$53 million till date (translating to c.5x+ MOIC) while Sixth Sense stands to make c.7x MOIC on its investment. (June 26, 2024)

[Expected] TA Associates, a US-based private equity firm, is looking to acquire a c.12% stake in Vastu Housing Finance, a mortgage lender, for c.$150 million along with existing investors like Norwest Venture Partners, from Multiples Alternate Asset. (June 26, 2024)

[Expected] Faering Capital, a PE firm, is looking to invest c.$25 million in Hangyo Ice Creams, a South India-based ice cream brand. (June 25, 2024)

Credit Deals and Issuances

ICICI Bank raised c.$360 million through 10-year infrastructure bonds at a coupon rate of 7.5%. (June 28, 2024)

upGrad, an ed-tech firm, raised c.$35 million in debt funding from EvolutionX, a technology-focused private credit fund. (June 28, 2024)

SBI raised c.$1.2 billion through the issuance of the first debt infrastructure bonds at a coupon rate of 7.4%. (June 27, 2024)

RBL, an Indian private bank, is looking to raise c.$780 million through a combination of QIP of shares and debt sale via private placement. (June 27, 2024)

Celebal Technologies, an IT services provider backed by Norwest Venture Partners, raised an undisclosed debt from BlackSoil, an alternative credit platform. (June 27, 2024)

Mindspace Business Parks REIT, a real estate investment trust by Mindspace, raised c.$150 million in debt from IFC by issuing sustainability-linked bonds at an annual coupon rate of 8%. (June 25, 2024)

KEY FUNDS AND FUNDRAISES

InvAscent, a healthcare-focused private equity firm, which earlier announced its first close in 2024, has increased the target corpus of its fourth fund to c.$325 million (vs c.$300 million earlier) and is looking to mark the final close by the end of the year. (June 26, 2024)

Cedar-IBSi Capital, a venture capital firm formed by Cedar Consulting and IBS Intelligence, a fintech market intelligence platform, secured a commitment from Hades Financial Private Capital Group, for its c.$30 million maiden VC fund launched in 2023. The first close was marked in March 2024. (June 25, 2024)

MARKET INSIGHTS & RESEARCH

Reports

Deloitte’s report: ‘Fuels of the future -Exploring alternative fuel options for transport’ highlights that in 2023, India surpassed Japan to become the third-largest light vehicle market, selling over 5 million units. The automotive sector, contributing 7.1% to India's GDP, is crucial to India's goal of becoming a $5 trillion economy by 2027. However, the sector's growth has increased dependence on global oil markets, highlighting the need for self-sufficiency and sustainable energy alternatives. India aims to achieve net-zero emissions by 2070 and reduce GHG emissions by 45% by 2030, driving the exploration of more environmentally friendly fuel options.

Technopack industry report on ‘Indian alco-beverage market’ gives insights into the Indian alco-bev market which stands at c.$37+ billion, making it one of the biggest markets in the world. The Indian spirit market is the second largest in the world. These are driven by the overall consumption trends and India’s disposable income per capita (c.6%+ CAGR) which grew faster than developed economies (c.3% CAGR). This report analyzes the market across various categories like alco-bev, wine, spirits, rum, brandy, beer and others.

Avendus Spark ‘Unique’orn series on ‘Indian textile sector’ shows that there are signs of volume recovery as global retailer inventory levels return to pre-COVID levels, though demand remains cautious. Indian cotton prices are competitive, driving growth for cotton spinners, with sector revenue up 8% yoy in 4QFY24. Home textile companies achieved 15%+ value growth, and garment manufacturers saw c.4% revenue growth. Cotton spinning companies reported robust margin expansion due to stable cotton prices and higher utilization. Despite competitive pricing pressures, government initiatives and potential trade agreements could boost the sector's growth in the medium term.

Ambit’s report on auto sector ‘Navigating the speed bumps’ highlights the "CODEC" framework for Auto OEMs that highlights a preference for tractors, two-wheelers (2Ws), and light-weight commercial vehicles (LCVs) due to favorable demand, stable competition, better earnings growth, and lower capex intensity. These segments are expected to see strong demand growth, with tractors, 2Ws, and LCVs witnessing significant CAGRs over the next few years. Passenger vehicles will experience a K-shaped recovery driven by SUVs, while medium and heavy commercial vehicles face muted growth. Profit margins are expected to see limited expansion, with 2Ws and tractors showing higher PAT growth. Electrification poses varying disruption risks, with 2Ws and LCVs most affected.

SBI’s research paper ‘The dichotomy of formalization’ highlights the formalization of India's informal sector, especially in rural areas. Unincorporated enterprises in services and trade have grown significantly, with rural establishments showing higher GVA growth compared to urban ones. Formal hired workers earn significantly more than informal workers, with services being the most remunerative sector. The informal economy has reduced from 26% in FY16 to 24% in FY23. The e-Shram portal has registered 300 million unorganized workers, indicating the potential for further formalization, though the pace has slowed in recent years.

‘CBRE’s 2024 India office occupier survey’ revealed key trends among corporate occupiers. There is a growing preference for an “office-first” approach, with 90% of occupiers favoring at least three days in the office per week. Long-term real estate strategies focus on portfolio expansion, while short-term strategies include flexible office use and quality upgrades. Workplace priorities include transformation, employee experience, sustainability, and technology. Additionally, one-third of companies plan to allocate 5% or more of their project budget towards ESG objectives.

Sector notes from ICRA:

Indian pharmaceutical industry: Stable outlook is expected driven by consistent demand in export and domestic markets. Revenue growth for Indian pharmaceutical companies is expected to moderate to 7-9% in FY2025. Key growth areas include US and emerging markets, with stable operating profit margins and robust financial health of scheduled commercial banks and non-banking financial companies.

Indian port & port logistics: Cargo volumes at ports are expected to grow by 6-8% YoY in FY2025, driven by healthy growth in container and coal segments despite risks from global economic slowdowns and geopolitical tensions. In FY2024, container and coal volumes grew by 11% and 8.7% YoY, respectively. New projects aligned with Maritime Vision 2030 and ongoing consolidation in the sector are expected to support future growth.

Articles

In June 2024, startups secured $1.7 billion in funding, a c.1.5x yoy increase. Zepto led with $665 million, followed by Creatio and Lenskart, each raising $200 million. In the last week of June, the deal value rose to $393 million from 22 rounds, up from $93 million the previous year. Read more.

Avendus’ note on ‘Will Arbitrage funds continue to enjoy tax arbitrage going forward?’ highlights that debt investments are taxed at higher rates than equities due to the higher risk associated with equity investments, warranting lower taxes for equity investors. Mutual funds with 65% or more in stocks are taxed like equities, but arbitrage funds, despite having low risk comparable to debt instruments, also enjoy these favorable equity tax rates. This tax advantage has led to significant growth in arbitrage funds and has diverted investments away from traditional debt instruments, impacting bank deposits and corporate borrowing costs.

Private credit funds, offering higher returns than public debt, have gained popularity globally, with the market surpassing $2.1 trillion in assets. In India, these funds saw significant growth, with over $2 billion raised in the latter half of 2023, and are projected to reach $60-70 billion in assets by 2028. However, fund operations need to be more transparent. Read more. [Paywall]

SEBI now permits up to 100% aggregate contribution by NRIs, OCIs, and Resident Indians in FPIs based in International Financial Services Centre (IFSCs). Applicants in IFSCs regulated by IFSCA must declare if these contributions will be 50% or more. As of March 2023, such investors held c.$42 billion in the Indian securities market. Read more. [Paywall]

KPIs

‘RBI’s Financial stability report’ states that the global economy faces risks from geopolitical tensions, high public debt, and slow disinflation, yet the financial system remains resilient. The Indian economy is robust, supported by stable financial conditions and sustained credit expansion. Scheduled commercial banks have strong capital ratios and low non-performing assets, while non-banking financial companies remain healthy with solid performance metrics. Read more. [Paywall]

India's fiscal deficit for April-May reached 3% of the FY25 target, c.$7 billion. The new government focuses on addressing agricultural distress, job creation, sustaining capital expenditure, and enhancing revenue growth for fiscal consolidation. S&P upgraded India's sovereign rating outlook to positive, contingent on fiscal discipline.

RBI highlighted rising household financial liabilities post-Covid, with overall savings dropping to 18.4% of GDP in FY23 from an average of 20% between 2013-22. Household debt, driven by increased retail loans, is mostly held by prime credit quality borrowers. Savings are now shifting towards physical assets and non-bank investments.

Consumption growth has been weak since the pandemic and is recovering slowly. Private consumption grew by 4% in the quarter ended March 31, 2024, compared to 1.5% a year ago, but it is still below the pre-pandemic average of 6.3% in 2019.

The government's total gross liabilities increased to c.$2.1 trillion by March 2024, up from c.$2 trillion in December, with public debt making up 90% and rising by 3.4% in Q4 2023-24. Indian bond yields softened due to fiscal adjustments, while US treasury yields remained volatile, and ownership patterns of securities shifted.

State governments and Union Territories plan to raise c.$32 billion through bond sales in July-September, while the Centre aims to raise c.$31 billion through Treasury Bills. The RBI will conduct 13 sets of auctions for state bonds and manage the central and state debt. Read more.

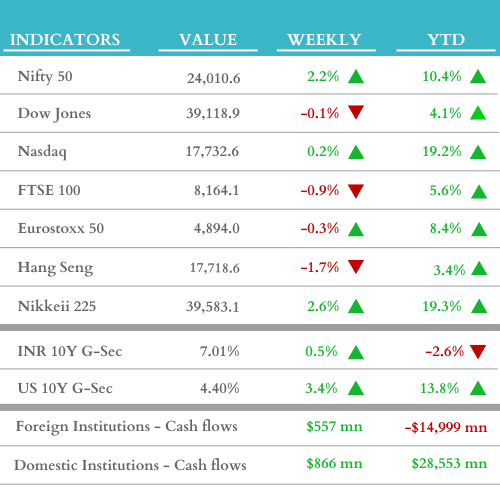

WEEKLY MARKET UPDATE (w/c June 24, 2024)

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.