India In Sight #66

Weekly updates on Indian private markets. Featuring India Private Credit 1H2024 report by EY.

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity. Deeply embedded in the private markets ecosystem, ACP works with large global institutions to provide creative capital solutions for companies and asset managers.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs, and top tier research

Search, screen, filter, and save - all reports at one spot! Subscribe to India In Sight Library

Subscribe to receive the newsletter every week in your inbox! Stay informed, stay ahead!

Key reports in this edition:

Private Credit India 1H 2024 by EY

Insights for the private capital ecosystem in India by Grant Thornton

Indian chemical industry’s outlook compendium 2024 by Indian Chemical News

India EMS: Tech boom to create new global leaders by Nomura

Monthly Dealtracker August 2024 by Grant Thornton

State of Household Finances by Care Edge

KEY DEALS

Equity

Onsurity, a subscription-based employee healthcare provider, raised c.$45 million in a Series B funding round led by Creagis. Other investors include IFC, Nexus Venture Partners and Quona Capital. (September 16, 2024)

Northern Arc Capital, a non-banking lender, secured c.$28 million from multiple investors including SBI General Insurance Company, SBI Life Insurance Company, Reliance General Insurance Company, Kotak Mahindra Life Insurance Company, Goldman Sachs, Societe Generale and Quant Mutual Fund ahead of its IPO. (September 14, 2024)

Centricity, a wealthtech startup, raised c.$20 million at c.$125 million valuation in a seed funding round led by Lightspeed India Partners. Other investors include Burman Family Office and Shantanu Agarwal. (September 12, 2024)

Allianz Capital, an asset management arm of the Allianz Group, to sell its c.14% stake in Interise, an Indian InvIt, to OMERS for c.$226 million. Allianz will also sell 25% stake in Interise Investment Managers to OMERS. (September 11, 2024)

Flexiloans, an MSME focused lending startup, raised c.$35 million in a Series C funding round from Accion, Nuveen, and Fundamentum. (September 11, 2024)

EQT to acquire a controlling stake in GeBBS, a healthcare technology service company, from ChrysCapital for an estimated c.$800 million. ChrysCapital acquired c.75% stake in the company in 2018 for a valuation c.$140 million (5x+ MOIC in <6 years). (September 09, 2024)

CA Magnum Holdings, an investment affiliate of Carlyle, to sell its stake in Hexaware Technologies, a technology and business process services company, in its upcoming IPO for c.$1.2 billion. (September 07, 2024)

[Exit] Peak XV, Stellaris Ventures, Sofina Ventures, and Fireside Ventures collectively sold their shares worth c.$190 million in Honasa Consumer, the parent company of MamaEarth, a skincare and beauty brand, in a bulk deal. (September 13, 2024)

[Expected] The promoters of Alkem Laboratories, a domestic drug and pharma company, are looking to sell a substantial stake in the company to private equity firms. (September 13, 2024)

Other Credit Deals and Issuances

Biocon Biologics is looking to raise c.$950 million through issuance of overseas bonds. The funds will be used to refinance the acquisition of Viatris Inc. (September 14, 2024)

Vastu Housing Finance, a home loan lender, raised c.$50 million in debt from US DFC in the form of ECB for 20 years. (September 12, 2024)

Slice, a consumer lending and payments startup, to raise c.$35 million in convertible debt from multiple domestic family offices. Other investors include Blume Ventures and 8i Ventures. (September 11, 2024)

InMobi, an advertising technology unicorn, secured c.$100 million in debt from Mars Growth Capital, a joint venture between MUFG and Liquidity Group. (September 11, 2024)

SBI is looking to raise c.$900 million through issuance of tier-2 bonds at c.7% coupon rate. (September 11, 2024)

Indian Bank is looking to raise c.$600 million through issuance of infrastructure bonds. (September 11, 2024)

IndusInd International Holdings (IIHL), a Hinduja Group company, to raise c.$360 million through issuance of NCDs. (September 09, 2024)

MARKET INSIGHTS & RESEARCH

Reports

EY’s report on ‘Private Credit India 1H 2024’ shows that private credit deal value is expected to exceed c.$10 billion in 2024 (vs $8.6 billion in 2023), with c.$6 billion in deal value recorded during 1H 2024 across 96 deals, majorly in real estate, infrastructure, and healthcare sectors. Domestic funds are gaining market share, driven by local expertise and lower-cost capital as global funds’ share fell to 53% in 1H 2024.

Grant Thornton report on ‘Insights for the private capital ecosystem in India’ views that India's potential in PE is driven by its growing economy, public markets, and focus on ESG, tech, and sustainable investments. Q2 2024 saw an 8% increase in deal value and a 9% increase in volume, witnessing 22 high-value deals ($100+ million) in Q2 alone. 86% of investors expect a higher global allocation to India.

This compendium on ‘Indian chemical industry’s outlook 2024’ outlines that the Indian chemical industry (valued at $212 billion in 2022) is expected to grow at a 9%+ CAGR. Increasing focus on specialty chemicals, ESG, and digital tech are key growth drivers. The industry also benefits from favorable policies like the PLI scheme, positioning India as a global chemical manufacturing hub.

Nomura’s report on ‘India’s Electronic Manufacturing Services (EMS)’ highlights India’s potential to become a global leader in EMS sector, growing from $115 billion in FY24 to $450 billion by FY30 at 25% CAGR, driven by PLI schemes, reduced dependency on imports, and growing markets. Key areas include mobile assembly, IT hardware, semiconductors, and component manufacturing.

Grant Thornton’s ‘Monthly Dealtracker for August’ highlights India's strong deal activity with 179 deals worth c.$8.7 billion, up by 63% vs July. Key sectors like telecom, banking, energy, and automotive saw notable M&A and fundraising, including 8 IPOs and 11 QIPs raising c.$3.4 billion. PE also gained momentum with 122 deals worth c.$2.5 billion, reflecting investor confidence, particularly in EVs.

Care Edge Ratings’ report on ‘State of Household Finances’ revealed that India's rising household debt is primarily driven by housing loans, which account for 50%+ of retail loans. Household debt stood at 38% of GDP in FY2023 (peak of 39.2% in FY21). This is comparable to its peers like Brazil (35%) and South Africa (34%) while Thailand (87%), Malaysia (67%) and China (62%) have higher debt.

ICICI Securities’ report on ‘Telecom sector’ analyzes the effects of recent tariff hikes on revenue and Adjusted Gross Revenue (AGR) market share. Operators are adjusting data plans to drive ARPU growth, by limiting unlimited 5G data plans. Higher AGR market share implies higher FCF which helps in strengthening balance sheet since telecom services business involve significant investments.

Deloitte’s report on ‘India’s economic outlook - Aug 2024’ outlines that India's GDP grew by 8.15% in FY2023-24 and is expected to grow at c.7.0% for 2024-2025, supported by improved capital flows and reduced inflation. Rural consumption is rising along with healthcare costs while education spending is declining.

PWC’s report on ‘The world of World Heritage sites’ provides a comprehensive overview of the process and significance of achieving UNESCO World Heritage status. It traces India’s involvement and highlights the benefits of heritage inscription, the role of digital transformation, and the need for innovative policies.

Articles

India is becoming a preferred destination for global investors. Funds like OTPP are focusing on inflation-protected and sustainable growth investments in India. Significant investments continue to flow in renewable energy, healthcare, and fintech, emphasizing a long-term approach to scaling assets. Read more.

India's economy has been leading global growth with an average GDP growth of 8.3% from 2021-2023, and 6.7% expected growth through 2024-2026. The country's stability is bolstered by low external debt, increasing foreign reserves, policy reforms, global supply chain diversification, clean energy, and tech. Read more.

SEBI is investigating the use of side letters or contribution agreements that provide preferential terms to certain limited partners (LPs) in venture funds. LPs have raised concerns about fairness in how VC funds treat different investors, including HNIs, family offices, and institutional investors. If SEBI prohibits side letters, it could hinder large funding rounds for startups and make it difficult for Indian VC funds to raise substantial corpuses. Read more. [Paywall]

KPIs

The Indian government remains committed to reducing the budget deficit despite challenges from coalition governance. Fitch Ratings highlighted India's focus on fiscal consolidation, with a reduced fiscal deficit target of 4.9% for this fiscal year and expectations for the debt-to-GDP ratio to decline between 2024 and 2026. [Paywall]

The Ministry of Statistics and Programme Implementation (MoSPI) plans to introduce district-level economic estimates by January next year through the use of web-based surveys and state collaboration. Currently, only state-level data like GSDP is available, but this initiative aims to provide more granular data at the national, state, and district levels. Read more.

The government is set to launch multiple enterprise-related surveys, including an annual survey to track private sector capital investments and an economic census. The capex survey will monitor yearly private sector capital spending to provide insights into investment trends. [Paywall]

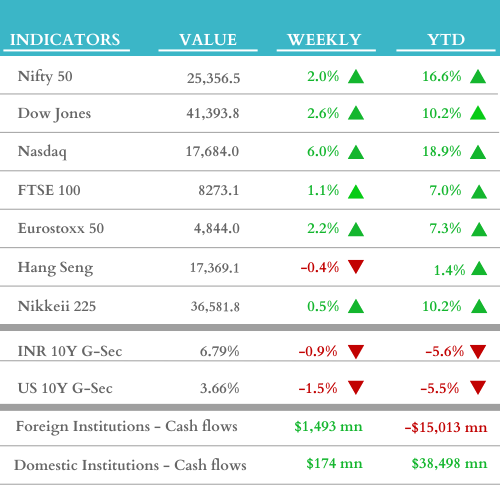

WEEKLY MARKET UPDATE (w/c September 9, 2024)

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.