India In Sight #95

Weekly updates on Indian private markets. Featuring 'Impact Analysis of US Reciprocal Tariff on India' by FICCI and 'The Running Yield' by Phillip Capital.

We are Ambassador Capital Partners, an investment firm with a focus on private credit and private equity.

In the spirit of making Indian private markets more accessible and transparent to global LPs and GPs, we have launched ‘India In Sight’ – consolidating and curating relevant information and insights from Indian private markets including trends, key deals, fundraises, KPIs, and top tier research

Search, screen, filter, and save - all reports at one spot! Subscribe to India In Sight Library

Subscribe to receive the newsletter every week in your inbox! Stay informed, stay ahead!

Key reports in this edition:

KEY DEALS

Equity

Eloelo, a social gaming and live streaming platform, raised c.$13 million in its Series B funding round led by Play Ventures. Other investors include Gameskraft Technologies, Kalaari Capital, and Waterbridge. (April 10, 2025)

Tessell, an enterprise cloud data startup, raised c.$60 million in its Series B funding round led by WestBridge Capital. Other investors include Lightspeed Venture Partners, B37.vc, and Rocketship.vc. (April 10, 2025)

Mosaic Wellness, a health and wellness startup, raised c.$20 million from Think Investment. (April 10, 2025)

Xindus, a trade-enablement startup, raised c.$10 million in a funding round led by 3one4 Capital. Other investors include Orios Venture Partners, Shastra VC and Caret Capital. (April 10, 2025)

Bose Corp, a global electronics player, invested c.$20 million in Noise, a gadget and wearable brand. (April 09, 2025)

Juspay, a payment technology company, raised c.$60 million in its Series D funding round led by Kedaara Capital. Other investors include SoftBank and Accel. (April 07, 2025)

Easebuzz, a digital payments company, raised c.$30 million in a funding round led by Bessemer Venture Partners, with plans to IPO in 2-3 years. (April 07, 2025)

Innovist, the parent company of D2C brand Bare Anatomy, raised c.$16 million in its Series B funding round led by ICICI Venture. Other investors include Mirabilis Investment Trust, Niveshaay Investment, and Sauce. (April 07, 2025)

HDFC Capital, the real estate PE arm of HDFC Group, launched a real estate development platform in partnership with Eldeco Group, a North India-based real estate developer, to develop 18 residential projects in tier II-III towns across various states, with HDFC Capital investing c.$175 million in the platform. (April 13, 2025)

Wakefit, a home furniture and sleep solutions company, is looking to raise c.$200 million ahead of its IPO. (April 10, 2025)

[Expected] Urban Company, a home services marketplace, to raise c.$60 million in primary capital via an IPO. (April 10, 2025)

[Expected] Seekho. a learning-focused OTT platform, is looking to raise c.$25-30 million from PEVC funds. (April 09, 2025)

[Expected] Bluestone, an omnichannel jewellery retailer, to raise c.$119 million via its IPO. (April 08, 2025)

[Expected] Aye Finance, a microlending platform, to raise c.$170 million via its IPO. (April 08, 2025)

[Expected] Scripbox, a wealthtech platform, is looking to raise c.$20 million at an expected valuation of c.$200 million (last round raised at c.$138 million valuation). (April 08, 2025)

KEY FUNDS AND FUNDRAISES

Expert Dojo, an early-stage VC and accelerator, raised c.$15 million to invest in Indian startups, with a target corpus of c.$100 million for its third global fund. (April 11, 2025)

Neo Asset Management, marked the first close of its second private credit fund at c.$235 million. The fund has a target corpus of c.$580 million. (April 11, 2025)

MARKET INSIGHTS & RESEARCH

Reports

FICCI’s ‘Impact Analysis of US Reciprocal Tariff on India’ summarizes the 26% reciprocal tariffs, impacting India’s ~$42B trade with US. Key sectors affected include marine products (esp. shrimp), honey, basmati rice, and processed foods (losing cost advantage to Latin American rivals). Relative tariff advantages in apparel, cashews, and electronics (e.g., smartphones) offer opportunities, as India faces lower duties than China, Vietnam, and Thailand. Pharma remains exempt, while steel, aluminium, and autos continue to face 25% tariffs. India engaging in bilateral talks to mitigate the impact.

Phillip Capital’s report ‘The Running Yield’ highlights easing liquidity, stable CAD (~1% of GDP), and strong forex reserves at ~$659B as supportive for Indian bond markets. INR has pulled back from 87.8 (Feb) to 85.5/USD. With RBI initiating rate cuts in Feb and another expected in April, 10-year G-Sec yields (~6.5%) and AAA corporate bonds (7.3–7.4%) offer attractive entry points.

Axis Capital’s report on ‘India EMS sector’ highlights India’s rapid rise as a global EMS hub, led by strong policy support (PLI, PMP, tax cuts) and mobiles (44% of domestic output; 59% of exports). India’s electronics output is projected to hit $500B by FY30 (30% from components). Mobiles saw 22% CAGR over FY21–25, with 99% localization in assembly but only ~15% value addition—set to rise to 40–50% through new components policy. In RACs, local value addition has risen from 30% to 70% (FY19–25), and expected to reach 90% by FY27, with PLI-driven investments.

Nuvama’s report ‘GLP-1s: A Weighty Affair’ details that GLP-1 drugs, originally used for diabetes, have rapidly emerged as a blockbuster category in obesity treatment (global market of $150–175B by 2035). India could benefit from the push for oral and generic versions. The Indian weight management market alone is expected to double to $56B by 2033, creating a opportunities for domestic pharma players.

Worldline’s report ‘India Digital Payments Report 2H 2024’ outlines that India’s digital payments ecosystem saw robust growth, led by UPI (up 42% YoY to 93.2B), with P2M volumes growing 50% and average ticket sizes declining. POS terminals reached 10M mark (23% growth), while UPI QRs grew 126% to 633M, reflecting rapid merchant adoption. Mobile app transactions jumped 41% in volume and 30% in value.

PWC’s report on ‘Sustainable packaging in the FMCG and retail’ states that India generates 26K tonnes of plastic waste daily, with only 9% globally recycled. In response, FMCG and retail players are integrating sustainable packaging aligning ESG goals with profitability and consumer expectations. ~70% of Indian consumers now prefer eco-friendly packaging.

Motilal Oswal’s report on ‘Trump tariffs’ highlights that amid global tariff risks and weak exports, FY25 Nifty EPS was cut by ~3%, though FY26 is expected to rebound with 14% earnings growth. India remains relatively less impacted by US tariffs compared to peers like China and Vietnam, and is backed by proactive policy measures including a 25bps repo rate cut, CRR reduction, and ₹1T tax stimulus.

CBRE’s ‘India Residential Market Monitor Q1 2025’ highlights that Q1 2025 saw balanced apartment sales (~66K) matching ~65K new launches. High-end and premium segments made up ~40% of total sales and ~44% of new launches, highlighting a shift toward upper-mid and premium housing. Favorable demand, RBI’s monetary easing, and narrowing EMI-to-rent gaps to drive momentum.

Articles

Indian bond yields are unlikely to remain fully insulated if US yields spike amid global uncertainty. While Indian yields may react less sharply, a significant rise in US yields (e.g., to 5%) could still lead to short-term upward pressure on Indian yields. Read more.

Fintechs and banks have appealed to end the Zero MDR regime and introduce a 0.3% fee on UPI transactions above ₹2,000 for merchants with over ₹20 lakh annual turnover. Concerns persist that such charges may eventually be passed on to consumers. [Paywall] Read more.

Gold has delivered stellar returns—33% in one year and 49% over two—but experts now advise caution. Given its role as portfolio insurance and a 30% divergence from equities, this could be the time to book profits and rebalance into other assets (equities, silver). Read more.

Gen AI is rapidly transforming digital marketing and customer engagement by enabling hyper-personalised campaigns, automated content creation, predictive analytics, and real-time multilingual communication. To fully leverage its potential, businesses must integrate gen AI with existing systems. Read more.

KPIs

Moody's revised India's 2025 growth forecast downward to 6.1%, citing risks from potential U.S. tariffs, despite a temporary pause. Sectors like gems and jewellery, medical devices, and textiles are expected to bear the brunt. RBI cut the repo rate and shifted to an accommodative stance to cushion the impact.

India’s WPI inflation is expected to ease to 2.1% in March 2025, driven by a seasonal decline in food prices, especially vegetables. While edible oil and sugar prices rose slightly, falling fuel costs are likely to support overall moderation.

Rising US tariffs have complicated the outlook for India’s economic growth. Despite signs of improvement, growth remains below target. The MPC has lowered the FY26 GDP growth forecast by 20 bps to 6.5%.

The RBI has cut the repo rate by 25 basis points to 6% and shifted its stance to 'accommodative' to support economic growth amid global uncertainties. The SDF rate now stands at 5.75% and the MSF rate at 6.25%.

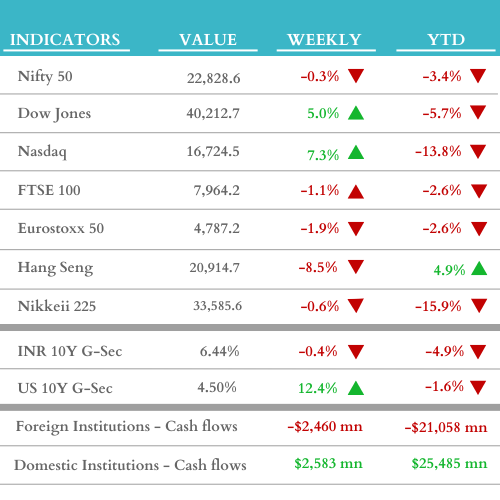

WEEKLY MARKET UPDATE (w/c April 07, 2025)

Check out India In Sight Library, a live repository focused on Indian private markets and alternative assets. It features a collection of 1,000+ research reports and articles from 250+ sources across 5 categories and 50+ sub-categories. Get your access now!

Thank you for reading India In Sight!

Read our other editions here.

Disclaimer:

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.